Early Signs and Challenges in Detecting Accounting Fraud in Companies

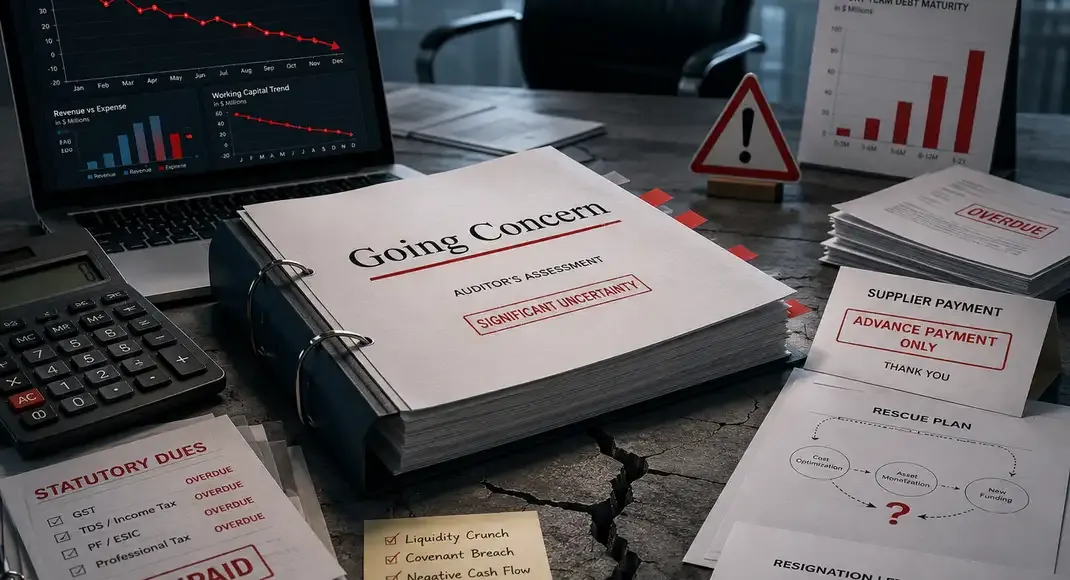

Accounting fraud often becomes evident only after several quarters, typically when a 'going-concern' warning appears in audit reports. Early indicators include profits reported alongside negative operating cash flow, short-term borrowings used for long-term assets, suppliers demanding advance payments, delayed statutory dues, and auditor resignations. The analysis suggests using these signals as a checklist and emphasizes that rescue plans should be critically tested rather than accepted, noting that prolonged discussions may indicate uncertainty rather than resolution.

First-hand measurement across 2 sources

We measured how 2 outlets covered this story. Coverage leans balanced overall (Left 0%, Centre 100%, Right 0%). Overall sentiment is negative (30/100). Lens Score 24/100 — low public interest.

Outlets analysed (first-hand measurement by TBN's Bias Engine):

- economictimes— balanced framing, negative sentiment

- economictimes— balanced framing, negative sentiment

AI Analysis

The articles focus on financial and auditing practices without political framing. They present a technical perspective on accounting fraud, highlighting systemic issues involving companies, auditors, and shareholders. The coverage is neutral, emphasizing procedural and financial signals rather than political or ideological viewpoints.

The tone across the articles is cautionary and analytical, highlighting risks and warning signs related to accounting fraud. While the content points to problems and uncertainties, it remains factual and avoids emotional or sensational language, maintaining a balanced and informative sentiment.

How 2 sources covered this story

Each source's own headline, political lean, and sentiment — so you can see framing differences at a glance.